Are you buying your first property? Chances are, you're wondering whether you should get an HDB loan or bank loan, and what the differences between the two are.

To get a better understanding of which loan is more suitable for you, our friends at 99.co break it down for us.

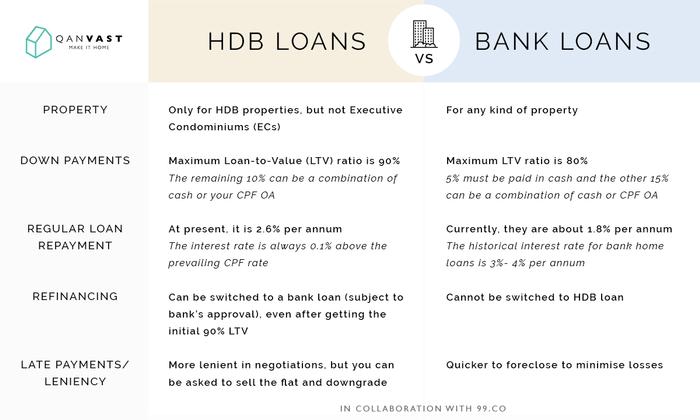

Property Type

Interior Designer: Inzz Studio

HDB Concessionary Loans are only for HDB properties, whereas bank loans can be used for any kind of property. Do note that for Executive Condominiums (ECs), there are no HDB loans, so you'll need a bank loan for that.

Down Payments

Interior Designer: erstudio

The maximum Loan-to-Value (LTV) ratio for HDB Concessionary Loans is 90 per cent (i.e. you can borrow up to 90 per cent of your flat’s value or price, whichever is lower). The remaining 10 per cent, can be paid with a combination of cash or using your CPF OA.

For banks, the maximum LTV ratio is 80 per cent. Five per cent must be paid in cash while the other 15 per cent can be paid with a combination of cash or your CPF OA.

Regular Loan Repayments

Interior Designer: Aiden-T

The current interest rate on HDB Concessionary Loans is 2.6 per cent per annum (always 0.1 per cent above the prevailing CPF rate).

Bank loan rates are more variable, unlike HDB Concessionary Loan rates, which almost never change; there is no perpetual fixed rate home loan in Singapore and bank interest rates are mainly determined in three ways:

- Singapore Interbank Offered Rate (SIBOR) loan packages

- Swap Offer Rate (SOR) loan packages (rare today)

- Internal Board Rate (IBR or BR) loan packages

Interior Designer: Fatema Design Studio

For SIBOR packages, the interest rate is the prevailing SIBOR rate plus the bank’s spread. For example, “3M SIBOR + 0.75” means the interest rate is the prevailing three month SIBOR rate, plus 0.75 per cent charged by the bank (the spread).

Every three months, when the SIBOR rate changes, the interest rate will be changed to match it - if you have a 1M SIBOR rate, the loan repayment amount will change every month, and if you ave a 3M SIBOR rate, then your loan repayment amount will change every three months.

Interior Designer: Create

SOR-based loan packages are similar, but based on the US and Singapore dollar exchange rate, instead of SIBOR. These packages are rare, and interest rates are much more volatile than SIBOR.

IBR or BR loan packages have interest rates set by the bank. For example, a Fixed Deposit Home Rate (FHR) loan has an interest rate that is pegged to the bank’s fixed deposit rates.

Why are bank loans cheaper?

Interior Designer: Fuse Concept

The historical interest rate for bank home loans is between three to four per cent per annum, which is more expensive than HDB loans.

However, due to the Global Financial Crisis in 2008, bank interest rates have been at record lows for almost 10 years. Currently, bank loans are around 1.8 per cent per annum, as opposed to HDB’s 2.6 per cent.

But this may not last, as interest rates are normalising after the crisis.

Dollar comparisons for a $350,000 flat

Interior Designer: Team Interior Design

HDB Loan

- Maximum loan quantum of $315,000

- Down payment of $35,000 (combination of cash of CPF OA)

- On a 25 year loan tenure, at 2.6 per cent per annum, monthly repayments = $1,429 per month

Bank Loan

- Maximum loan quantum of $280,000

- Down payment of $70,000. Of this amount, up to $52,500 can come from CPF OA. A minimum cash payment of $17,500 is required.

- On a 25 year loan tenure, assuming an interest rate of 1.8 per cent per annum*, monthly repayments = $1,159.72 per month

*This is based on current, typical loan rates. We cannot assume that the bank interest rates will remain at this level over 25 years.

Switching from HDB to bank loans

Interior Designer: Fifth Avenue Interior

You can refinance your HDB loan into a bank loan (subject to the bank’s approval), even after getting the initial 90 per cent LTV. Your bank loan, however, cannot be refinanced into an HDB loan.

Late Payments & Leniency

Interior Designer: D Initial Concept

HDB's main aim is to provide the public with housing, whereas the bank's would be to find profits for its stakeholders and shareholders.

If you are unable to pay your home loan, HDB is more lenient in negotiations (but this doesn’t mean you can get away without paying your home loan – you can still be asked to sell the flat and downgrade!).

Banks are quicker to foreclose and minimise their losses.

Which loan is better for me?

Architect: UPSTAIRS_

If you’re on a tight budget...

HDB loans should be considered first, as there is a smaller cash outlay. If you find the interest rate too high, you always have the option of refinancing to a bank loan later on.

If you intend to upgrade from an HDB to private property fast...

Consider a bank loan, or quickly refinancing into a bank loan from an HDB loan. This could reduce monthly repayments, minimising the interest eating into your resale gains.

Interior Designer: ID Gallery

Of course, everyone's situation is different, so speak to a qualified, independent mortgage broker for personalised help. These services are usually free.

*This article was first published by property portal 99.co, with the largest number of active listings.*

Get a budget estimate before meeting IDs

Get a budget estimate before meeting IDs